- 1. What is CASA and Why Does It Matter?

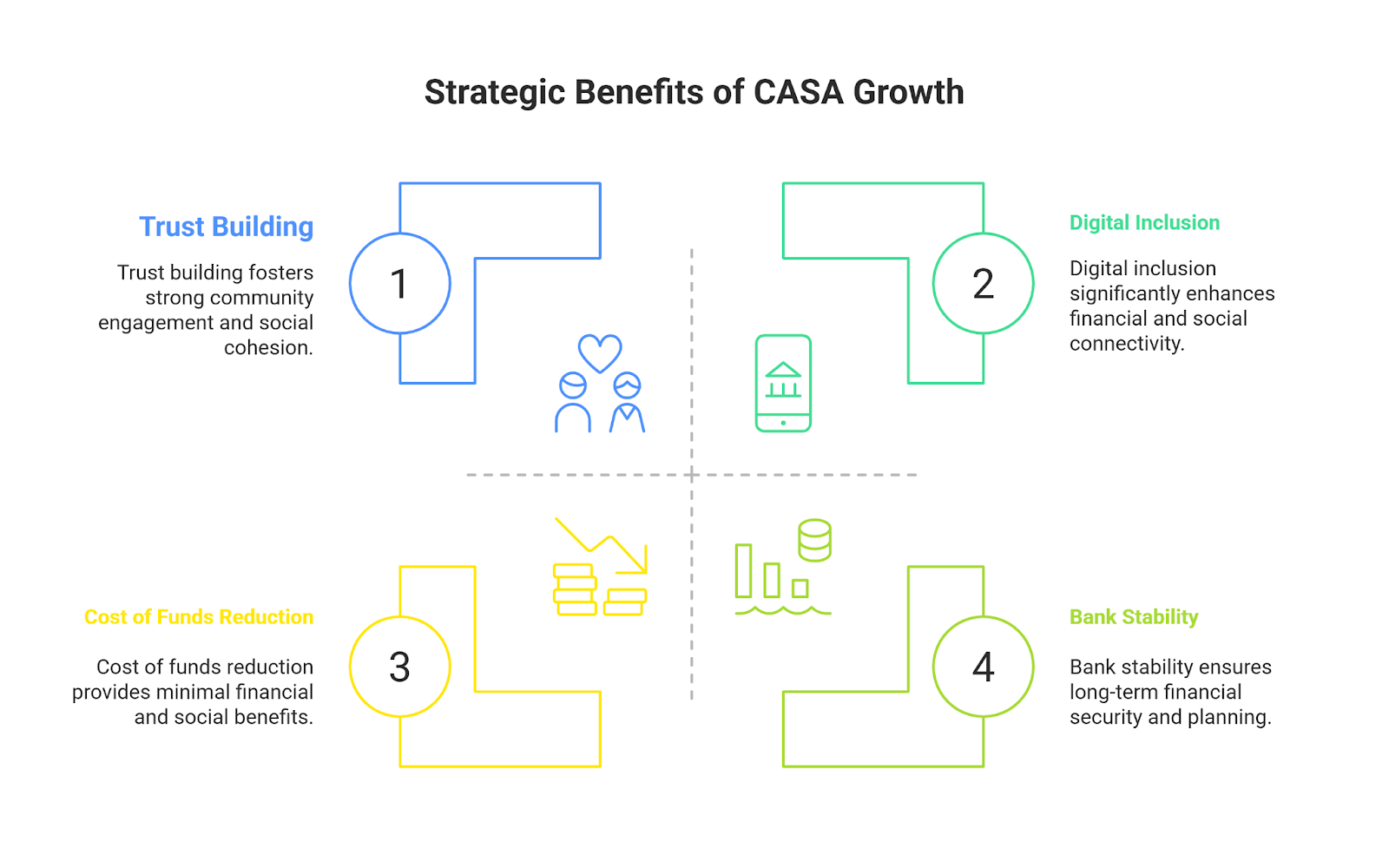

- 2. Reason 1: CASA Growth Lowers the Cost of Funds

- 3. Reason 2: It Builds Trust and Engagement with Citizens

- 4. Reason 3: CASA Strengthens Digital and Inclusive Banking

- 5. Reason 4: CASA Growth Boosts Bank Stability and Long-Term Planning

- 6. CASA Growth in Action: What Banks Can Do

- 7. The Bigger Picture: CASA Growth and India’s Development

- 8. Frequently Asked Questions

Highlights of the Blog

-

CASA growth reduces the cost of funds for banks, enabling them to offer affordable credit to MSMEs, farmers, and underserved communities—directly supporting the goals of Viksit Bharat & EASE 7.0.

-

Active CASA engagement builds trust and financial inclusion, especially among women, small traders, and rural populations, bringing them closer to the formal and digital economy.

-

A strong CASA base enhances banking system stability, allowing long-term planning, digital innovation, and efficient delivery of government benefits through Direct Benefit Transfers (DBT).

Did you know that one of the strongest indicators of a healthy banking system is a strong CASA base? CASA stands for Current Account Savings Account, and its growth plays a major role in improving financial stability, reducing cost of funds, and supporting inclusive development, exactly what Viksit Bharat & EASE 7.0 aim to achieve.

As India marches confidently towards a Viksit Bharat, Action Point 4 (AP 4) of EASE 7.0 highlights the importance of deepening customer engagement and improving deposit mobilisation through CASA growth. But why is it so critical for the future of banking in India?

Let’s break it down in a simple, friendly way.

What is CASA and Why Does It Matter?

Before we dive into the reasons, here’s a quick refresher. CASA refers to the Current and Savings Account deposits that customers maintain with a bank. These are low-cost funds, meaning banks don’t have to pay high interest on them.

A higher CASA ratio means a stronger base of stable, cheap funds which allows banks to lend more efficiently and support economic growth.

And that’s where Viksit Bharat & EASE 7.0 come in ensuring that every citizen, from cities to the most remote villages, becomes part of India’s financial growth story.

Reason 1: CASA Growth Lowers the Cost of Funds

For any bank, the cost of funds is a big deal. The more a bank pays for the money it lends, the more it must charge borrowers which slows down credit and development. CASA deposits, especially savings accounts, offer a much lower cost compared to fixed deposits or borrowed funds.

This means:

-

Banks can offer loans at better rates.

-

More people, especially in rural and semi-urban areas, can access affordable credit.

-

MSMEs and farmers benefit from cheaper working capital.

However, the FICCI–IBA Survey reports that 57% of banks have seen CASA deposits decline, as depositors increasingly shift toward higher-yielding fixed deposits when interest rates rise.

This trend poses a challenge for banks striving to maintain a low cost of funds and highlights the need for innovative strategies to retain CASA.

Viksit Bharat & EASE 7.0 focus on strengthening rural credit, MSME support, and financial inclusion. CASA growth directly fuels these goals by giving banks a cheaper and stable resource base.

Sustaining CASA growth is thus critical not only for bank profitability but also for accelerating India’s broader developmental goals under Viksit Bharat & EASE 7.0.

Reason 2: It Builds Trust and Engagement with Citizens

CASA accounts aren’t just about deposits. They are relationship accounts. People use them daily for saving, spending, transfers, and more. When banks promote CASA growth, they are not just collecting money they are building trust, habit, and regular engagement.

Under EASE 7.0 (AP 4), banks are encouraged to go beyond just account opening. The goal is to activate accounts, encourage transactions, and offer services that truly meet customer needs, especially women, senior citizens, small traders, and rural households.

This deep engagement:

-

Keeps customers connected to the banking system.

-

Increases financial literacy and confidence.

-

Brings people closer to the digital economy.

The growing scale of inclusion is evident. According to the Press Information Bureau, as of January 15, 2025, 54.58 crore Jan Dhan accounts have been opened—55.7% of them held by women. This reflects a significant rise in trust and participation, particularly among segments previously underserved.

All this supports the dream of a Viksit Bharat, where financial empowerment is not just a slogan, but a daily reality enabled through CASA engagement and EASE 7.0 reforms.

Reason 3: CASA Strengthens Digital and Inclusive Banking

India is going digital at a rapid pace, and so is banking. UPI, Aadhaar-enabled payments, DBT (Direct Benefit Transfers), and mobile wallets have changed how people use money. CASA accounts form the backbone of this digital financial ecosystem.

With CASA:

-

People receive subsidies, pensions, wages, and remittances directly.

-

They can pay bills, send money, and manage their finances on the go.

-

Rural and remote areas get connected to the mainstream economy.

Viksit Bharat & EASE 7.0 strongly promote digital inclusion. CASA growth ensures that people are not left behind in this transformation.

When more people maintain and use their savings and current accounts actively, they unlock access to insurance, credit, investments, and more.

And that’s the real meaning of inclusive development.

Fun Fact:

Over 90% of Indian villages now have digital banking access—thanks to CASA growth and Viksit Bharat & EASE 7.0—enabling even remote users to bank on their phones!

Reason 4: CASA Growth Boosts Bank Stability and Long-Term Planning

When banks have a strong CASA base, they don’t just survive—they thrive. These deposits are:

-

More predictable.

-

Less volatile.

-

Helpful in managing liquidity during tough times.

This stability gives banks the confidence to plan long-term:

-

Launch new credit schemes.

-

Invest in rural branches and infrastructure.

-

Innovate new digital solutions.

AP 4 of EASE 7.0 is all about improving deposit mobilisation, understanding local needs, and using technology to boost savings culture. CASA growth is not a one-time goal—it’s a long-term pillar for banks working towards a Viksit Bharat.

CASA Growth in Action: What Banks Can Do

To align with Viksit Bharat & EASE 7.0, banks are rolling out practical initiatives under AP 4 to encourage CASA growth:

-

Doorstep Banking – Reaching out to customers in villages and small towns to open and activate savings accounts.

-

Simplified Digital Onboarding – Quick account setup via mobile or Aadhaar-based systems.

-

Awareness Campaigns – Educating customers about the benefits of savings and digital banking.

-

Women-Centric Products – Encouraging women entrepreneurs and SHG members to open and use CASA accounts.

-

Special Drives – Targeted campaigns in low-CASA areas with branch-level goals and incentives.

Each of these steps contributes to a more robust, customer-friendly, and digitally ready banking environment, just what Viksit Bharat & EASE 7.0 envision.

The Bigger Picture: CASA Growth and India’s Development

As we think about India’s future where every citizen is empowered, every rupee is productively used, and every village is digitally connected. CASA growth becomes more than just a banking target, it becomes a national mission.

By strengthening CASA:

-

Banks become more resilient.

-

Citizens become more financially active.

-

The government can deliver welfare faster and more efficiently.

-

And the economy moves faster towards becoming truly Viksit Bharat.

The scale of this potential is already visible. As of April 9, 2025, PMJDY (Jan Dhan) deposits hit ₹2.63 lakh crore, spread across 552 million accounts, with an average balance of ₹4,760. This highlights the massive base of low-cost CASA funds that banks can leverage to support inclusive growth and efficient financial delivery.

EASE 7.0 gives the roadmap. CASA growth gives momentum. Together, they are key drivers of India’s journey toward a confident, connected, and financially empowered Viksit Bharat.

Final Thoughts

CASA growth might sound like a technical banking term, but its impact is deeply human. It touches the life of a farmer getting a subsidy, a student receiving a scholarship, a woman entrepreneur saving for her business, and a migrant worker sending money home.

That’s why under AP 4 of EASE 7.0, CASA isn’t just about money, it’s about trust, inclusion, and transformation.

Let’s support and spread awareness about CASA growth. Because when more Indians actively use their savings and current accounts, we all take one step closer to a Viksit Bharat.

If you are looking to automate your banking systems, check out business automation services from CBSL group today.

Frequently Asked Questions

1. What exactly is a CASA account, and why is it important for banks?

CASA stands for Current Account and Savings Account. These are low-interest deposits that provide banks with stable and low-cost funds.

A higher CASA ratio enables banks to offer loans at better rates and increases their ability to support inclusive lending and financial growth, aligning with EASE 7.0 and the vision of Viksit Bharat.

2. How does CASA growth support financial inclusion in rural areas?

CASA accounts are often the first point of contact with formal banking for rural populations. Through doorstep banking, Jan Dhan Yojana, and simplified onboarding, banks can help more citizens, especially women, small traders, and farmers actively participate in the financial system, improving inclusion and digital literacy.

3. Why is CASA preferred over fixed deposits or other sources of funds?

Unlike fixed deposits, which offer higher interest rates, CASA accounts offer minimal or no interest. This reduces the bank’s overall cost of funds, enabling more competitive lending and better financial health. It also provides greater liquidity and helps banks plan for long-term investments.

4. What role does CASA play in digital banking and DBT (Direct Benefit Transfer)?

Most DBT schemes, subsidies, pensions, and government benefits are credited directly into CASA accounts. These accounts also enable users to transact via UPI, mobile apps, and ATMs. CASA growth thus supports a cashless, connected India the key to EASE 7.0’s digital inclusion mission.

5. What are some strategies PSU banks are using to grow CASA under EASE 7.0 AP 4?

Under Action Point 4, banks are implementing strategies like:

-

Women-centric savings products

-

Doorstep banking in rural areas

-

Financial literacy campaigns

-

Digital onboarding using Aadhaar

-

Special branch-level CASA drives in underserved regions

These initiatives help deepen engagement, boost deposit mobilisation, and bring more citizens into the fold of Viksit Bharat.